Kalshi’s market on the removal of Ali Khamenei as supreme leader of Iran ended last weekend with the company taking a $2.2 million loss after a messy series of conflicting rule “clarifications.” For many traders, it raised questions about how the exchange handles large, controversial events.

But those questions would be magnified for one class of customer that Kalshi has been chasing lately: institutional Wall Street money.

Kalshi Khamenei market confusion

In January, Kalshi listed a contract titled “Ali Khamenei out as Supreme Leader?” A plain reading of the title would suggest that Khamenei’s death would settle the market for “yes.”

However, the terms and conditions said otherwise.

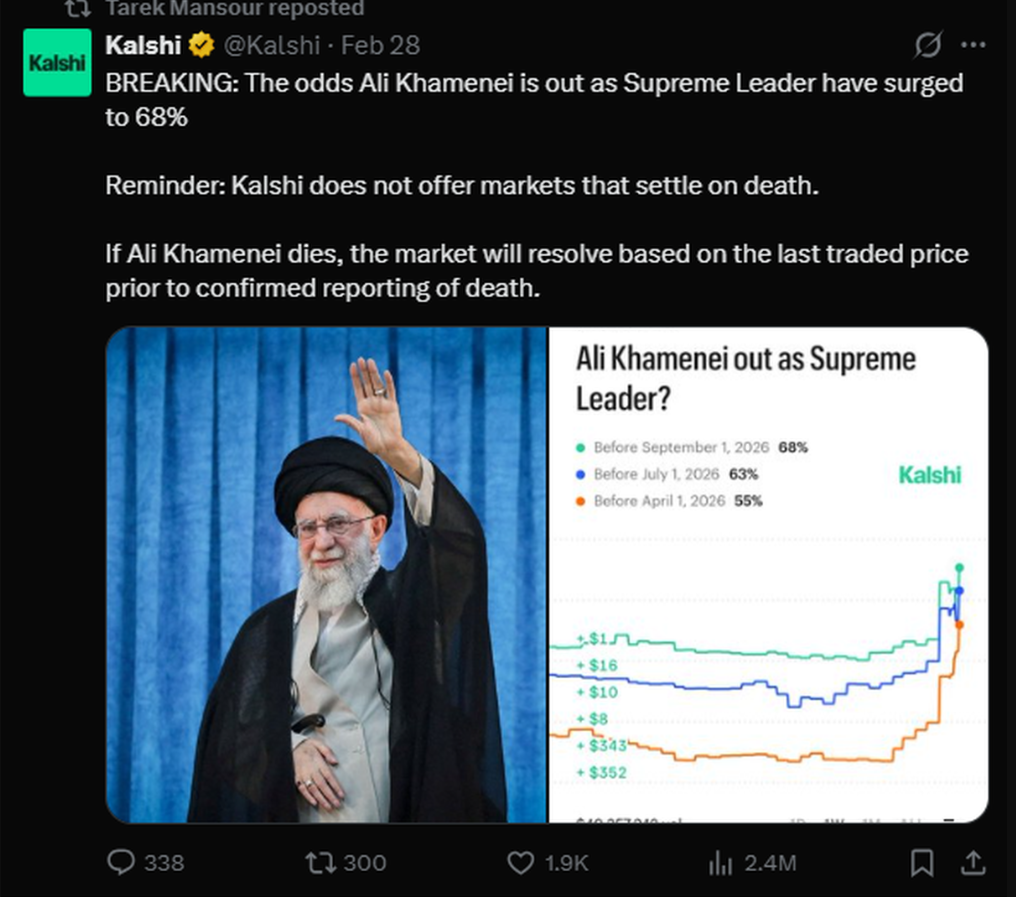

“If Ali Khamenei leaves solely because they have died, the associated market will resolve and the Exchange will determine the payouts to the holders of long and short positions based upon the last traded price (prior to the death),” they said. “If a last traded price is not available or is not logically consistent, or if the Exchange determines at its sole discretion that the last traded prices prior to death do not represent a fair settlement value, the Outcome Review Committee will be responsible for making a binding determination of fair allocation.”

Users were also able to bet on Khamenei leaving office in a “world leaders out” market, with similar rules.

That clause ensures that the market is not a contract on war, assassination, or terrorism, which Kalshi staff say would not be permitted.

Soon after midnight ET as Friday turned into Saturday, U.S. and Israeli forces began air strikes in Iran, and soon unconfirmed reports claimed that Khamenei had been killed.

But not only did trading continue through Saturday morning, Kalshi appeared to promote the market to customers who may have been unaware of how the market would settle if Khamenei died, listing it on its front page.

As more trades came in, Kalshi made more in fees. Had the fees not ultimately been reimbursed, Kalshi would have made around $500,000 in fees from the market.

Kalshi issued a clarification stating that if Khamenei died, the market would be settled at the last traded price following “confirmed reports” of his death, but this appeared to create more confusion, as the existing reports were not yet confirmed, so traders appeared to be able to manipulate the final settlement price by trading in the market before confirmation occurred.

Kalshi then posted on social media site X that the odds of his removal had surged to 68%, noting again that the market would resolve based on the price at the time of “confirmed reports” of Khamenei’s death. Kalshi CEO Tarek Mansour reposted it.

A later clarification addressed the “grammatical ambiguity” in the first, noting that the settlement would be based on the price before Khamenei’s death.

With traders upset, Kalshi ultimately settled the market at the price before strikes in Iran began, and reimbursed all contracts bought afterward. It also reimbursed all fees on the contracts. Mansour said the business took a $2.2 million loss on the market by doing so.

Kalshi courts institutional traders

All of that came just days after Kalshi looked to be breaking through to big-time fund managers, as founders Tarek Mansour and Luana Lopes Lara pursued their stated goal of creating an asset class worth trillions and rivaling the stock market. That means courting institutional clients such as big banks or hedge funds.

On Feb. 19, Kalshi partnered with Tradeweb, a global bond marketplace with $2.6 trillion in daily volume. Under that deal, Kalshi’s real-time event contract probabilities will be integrated into Tradeweb’s platforms for more than 3,000 institutional clients, with a second phase exploring a direct trading portal.

“We all know that new markets don’t succeed on concept alone,” Tradeweb CEO Billy Hult wrote about the deal on LinkedIn. “They require institutional-grade infrastructure: governance, connectivity, liquidity and trust.”

On Feb. 24, Bloomberg reported that Kalshi was hiring Andy Ross, formerly head of U.K. financial markets at Standard Chartered, to head up its institutional division, convincing Wall Street clients to trade on the platform and managing their needs.

Within days, the strikes in Iran began. For institutional funds, this kind of global uncertainty would have provided a need to hedge specific risks. For example, if a fund was long on oil due to global demand reasons, it may have wanted to hedge its oil trade with a bet on Iranian leadership being removed.

But instead, Kalshi’s markets on Feb. 28 showed the inherent tensions at play between Kalshi’s dream of prediction markets as a trillion-dollar asset class and the way the product actually exists right now.

Inconsistency raises questions

For institutional money, an important clarification buried in the rules is not a major problem as long as the rules are clear and consistent. And it was likely less-experienced traders who would have been most affected by the Khamenei market before refunds. Those traders would have been less likely to click into the rules document, and more likely to trade based on a surface-level reading of the market.

But the messy process that took place afterward is probably a bigger problem. Kalshi can’t take big losses refunding customers over every contentious market, and Wall Street funds want certainty.

The Khamenei settlement took roughly 19 hours from halt to formal close, included two clarifications, and ended with the exchange absorbing losses.

For institutional operations teams, the specifics of the death carveout matter less than the fact that a straightforward binary contract produced a settlement process that was improvised in public over the course of a day.

Funds that trade on CME or through Tradeweb expect contracts to settle according to their terms on a predictable timeline. The Khamenei market suggested Kalshi has not achieved that yet.

Timing of settlement causes problems

The situation also revealed the challenges of fully considering every possible outcome in markets where death can be a deciding factor.

Kalshi reacted to initial reports of Khamenei’s death by putting up a disclaimer explaining its settlement rules.

But that disclaimer said the market would be settled at the last traded price prior to “confirmed reporting of death.” And while Khamenei’s death was widely rumored, it was not yet confirmed.

Had that rule been enforced as written, Kalshi would have effectively paid out on Khamenei’s death, due to the spike in odds when his death was unconfirmed.

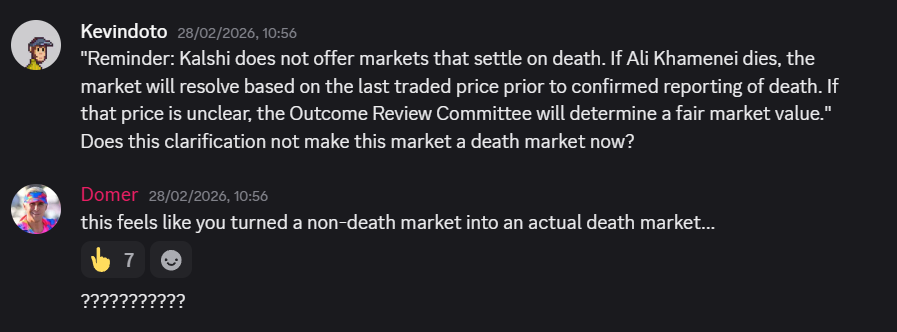

“This feels like you turned a non-death market into an actual death market,” prominent prediction market trader “Domer” wrote on Kalshi’s Discord channel.

Kalshi later issued a new clarification, calling the first one “grammatically ambiguous,” and saying the resolution price would be the last traded price prior to death. It ultimately resolved the market using the last traded price before strikes began.

Even that meant settling based on odds that were likely heavily based on the possibility that Khamenei died, particularly as aircraft and ship movements suggested U.S. military action in Iran could be coming soon. The price of Khamenei being out of office within the next 23 hours was a little under 2%.

It’s not always clear when to set as the cut-off point when the subject of a market dies, and it likely changes from contract to contract, but the inconsistency goes against the one thing big-money funds are looking for: in Hult’s words, “institutional-grade infrastructure: governance, connectivity, liquidity and trust.”

Kalshi’s markets team generally handles resolutions of contracts. Many of the markets it has to resolve are sports outcomes, where the result is almost always clear — though even these are not always resolved accurately. But alongside those markets are a handful of more ambiguous contracts, where more work is needed to resolve them.

Mansour’s defense

But the wider issue may be that many event contracts that would in theory be highly valuable to institutional funds are going to involve markets on death.

In an X post explaining the process over the weekend, Mansour defended offering the market.

“A market on Ali Khamenei out as Supreme Leader was important because leadership changes in Iran have major impact on the world order: geopolitical implications, economic consequences, national security considerations, oil and commodity prices, many of which move based on news and expectations around this outcome,” he wrote. “And it’s always possible for a ruler to step down or transition power without death, even in autocracies. It just happened in Venezuela.”

Those impacts are real, but they are likely most significant if a leader is removed by death, something that traders are not able to hedge.

Polymarket removes nuclear weapon market

Polymarket’s unregulated global site, free from the purview of the Commodity Futures Trading Commission (CFTC) that regulates Kalshi, took the other approach. It offered bets on Khamenei’s exit that settled for “yes” upon death, and has also taken bets on wars in Gaza and Ukraine.

Though even Polymarket has been inconsistent about when a contract is too distasteful.

The exchange had a long-running market on whether a nuclear weapon would detonate in 2026, including both tests and uses in war. But war in Iran made the connections between the market and real death much clearer, and made the market appear much more controversial. Amid negative publicity, Polymarket took down the nuclear weapon markets Tuesday.

Free from CFTC rules surrounding war or assassination, Polymarket’s global site can offer controversial markets as long as it can weather the public opinion storm. But Wall Street funds will almost certainly be reluctant to put their money into an unregulated platform, with little room for recourse if things go wrong. Polymarket’s issues with insider trading on politically sensitive markets also have the potential to keep Wall Street away. Trading based on insider knowledge is not banned by Polymarket’s global rulebook, and the exchange’s lack of identity checks means it does not know if its customers might have inside knowledge.

Kalshi’s regulatory status looked like a major advantage over its rival when it comes to onboarding institutional money, but its attempts to thread the needle of offering contracts on the biggest global events without directly letting users bet on death didn’t go according to plan.

That tension is at the heart of Kalshi’s challenge in becoming the stock-market-like asset class that it hopes to become. The Wall Street money needs to trade on the most world-changing events, but those events are often deeply linked to war or death.