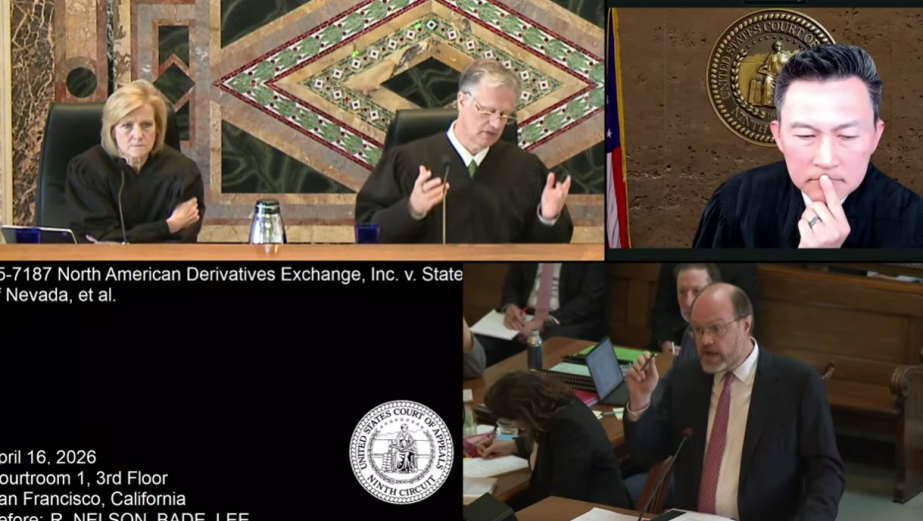

To the extent that a result can be divined from oral arguments, the Ninth Circuit hearing between Nevada and Kalshi, Crypto.com, and Robinhood on April 16 did not appear to go the prediction markets’ way.

Judge Ryan D. Nelson looked exasperated at the prediction markets’ arguments and told their lawyers “this can’t be a serious argument” at one point.

The one thing Nelson seemed to be especially concerned about was the CFTC’s rule 40.11:

§ 40.11 Review of event contracts based upon certain excluded commodities.

(a) Prohibition. A registered entity shall not list for trading or accept for clearing on or through the registered entity any of the following:

(1) An agreement, contract, transaction, or swap based upon an excluded commodity, as defined in Section 1a(19)(iv) of the Act, that involves, relates to, or references terrorism, assassination, war, gaming, or an activity that is unlawful under any State or Federal law; or

(2) An agreement, contract, transaction, or swap based upon an excluded commodity, as defined in Section 1a(19)(iv) of the Act, which involves, relates to, or references an activity that is similar to an activity enumerated in § 40.11(a)(1) of this part, and that the Commission determines, by rule or regulation, to be contrary to the public interest.

(b) [Reserved]

(c) 90-day review and approval of certain event contracts. The Commission may determine, based upon a review of the terms or conditions of a submission under § 40.2 or § 40.3, that an agreement, contract, transaction, or swap based on an excluded commodity, as defined in Section 1a(19)(iv) of the Act, which may involve, relate to, or reference an activity enumerated in § 40.11(a)(1) or § 40.11(a)(2), be subject to a 90-day review. The 90-day review shall commence from the date the Commission notifies the registered entity of a potential violation of § 40.11(a).

(1) The Commission shall request that a registered entity suspend the listing or trading of any agreement, contract, transaction, or swap based on an excluded commodity, as defined in Section 1a(19)(iv) of the Act, which may involve, relate to, or reference an activity enumerated in § 40.11(a)(1) or § 40.11(a)(2), during the Commission's 90-day review period. The Commission shall post on the Web site a notification of the intent to carry out a 90-day review.

(2) Final determination. The Commission shall issue an order approving or disapproving an agreement, contract, transaction, or swap that is subject to a 90-day review under § 40.11(c) not later than 90 days subsequent to the date that the Commission commences review, or if applicable, at the conclusion of such extended period agreed to or requested by the registered entity.

And in his view, the prediction markets didn’t have a good answer to it.

The rule refers to a “prohibition” on contracts involving gaming, as well as war, terrorism, assassination, and other illegal activities. Prediction market lawyers have argued that it’s not quite a blanket ban (though some public statements from Kalshi CEO Tarek Mansour seem to contradict this).

But the most literal reading of the text doesn’t help the prediction markets.

“No one has come up with a coherent, English reason why that shouldn’t be the rule. It says you cannot self-certify and post it,” Nelson said at one point in the heading.

The CFTC’s rule, not Congress’

There’s one thing that makes the whole discussion odd.

40.11 is a CFTC rule, not a statute from Congress. And the CFTC filed an amicus brief in this very case and is suing states to defend its jurisdiction over prediction markets.

So a lawyer for the agency that wrote the rule — and could amend or withdraw it — was standing across from Nelson as he argued the rule could cost prediction markets the case.

If we’re just talking about interpretation of statute, federal agencies don’t get much benefit of the doubt, following the 2025 Supreme Court decision Loper Bright Enterprises v. Raimondo.

But if we’re talking about a CFTC rule, is the agency’s own stance more important?

With that in mind, surely the CFTC could make this all irrelevant, right? Could it issue an interpretation of the rule, making it clear that sports event contracts don’t count? Or failing that, simply change or remove the rule?

It may be more difficult than it appears.

40.11 and the ‘special rule’

It’s important to understand the interaction between the CFTC’s rule 40.11 and the “special rule” in the Commodity Exchange Act — two rules that have very similar language, but some differences.

(C)Special rule for review and approval of event contracts and swaps contracts

(i)Event contracts

In connection with the listing of agreements, contracts, transactions, or swaps in excluded commodities that are based upon the occurrence, extent of an occurrence, or contingency (other than a change in the price, rate, value, or levels of a commodity described in section 1a(2)(i) [2] of this title), by a designated contract market or swap execution facility, the Commission may determine that such agreements, contracts, or transactions are contrary to the public interest if the agreements, contracts, or transactions involve—

(I)activity that is unlawful under any Federal or State law;

(II)terrorism;

(III)assassination;

(IV)war;

(V)gaming; or

(VI)other similar activity determined by the Commission, by rule or regulation, to be contrary to the public interest.

The special rule says that “the Commission may determine that such agreements, contracts, or transactions are contrary to the public interest” if they involve gaming, war, assassination, terrorism, or other illegal activities. A key word there is “may,” which implies a choice. Based just on the wording of the Commodity Exchange Act (CEA), the CFTC can permit any gaming, war, assassination, or terrorism contract — as long as it’s within the public interest.

But the wording of 40.11 is different.

The literal text reads much more like a blanket ban. Instead of a direct description of the CFTC making a two-part test, the text makes reference to a “prohibition” and says “a registered entity shall not list” contracts involving the enumerated categories.

Prediction markets have argued that it should still be read as a two-part test, with references to a 90-day review further down the rule hinting at a public interest component. But Nelson wasn’t convinced.

Two-part test or ban?

Whatever the wording of the rule says, in practice the CFTC appears to have enforced it more like a two-part test than a blanket ban.

When the agency wanted to ban Kalshi’s election contracts in 2023, it did not just argue that they involved gaming, but instead also laid out why it believed them to be against the public interest.

But if a rule is implementing a law from Congress, agencies have a requirement to enforce it.

So if judges interpret the rule as a blanket ban, the CFTC may not be able to enforce it as a two-part test.

Could it issue some kind of clarification, saying that actually the prediction markets are right, and the rule actually is describing a two-part test?

“I don’t think it would do any good,” an expert in commodity futures law told InGame. “There’s still a wisp of deference for their own regulations, but the court will consider how well thought through it is and how longstanding it would be. It would be pretty obvious that they just did it for the purpose of litigation if they did it now.

“The first word of it is prohibition. It would be hard to issue an interpretation that says it’s not.”

Do sports contracts involve gaming?

So how about clarification about what is and isn’t “gaming”?

When CFTC lawyer Jordan Minot spoke, he revealed for the first time the CFTC’s stance on whether contracts involving gaming includes sports contracts. His view was that it refers instead to contracts on “casino gaming.”

So how much does it matter that the CFTC itself doesn’t think sports contracts are included under 40.11?

The CFTC’s stance is that the word “involves” in the rule refers to the underlying activity that the contract is on — the election, or news event, or sports match that the event contract resolves based on the result of. And that “gaming” refers to games of chance, not sports games. It’s a position that was outlined in a letter that CFTC Chair Michael Selig worked on when employed by venture capital fund Paradigm.

But it sounds a little awkward when explained out loud to a skeptical judge.

Can the CFTC make its interpretation official? Could it write a guidance that says, “When it comes to Rule 40.11, gaming just means casino games” and leave sports event contracts in the clear?

Implementing rules

The problem here is that CFTC’s interpretation is at least partly tied to the CEA’s special rule.

40.11 is considered an implementing rule — a regulation issued by a federal agency to carry out a specific statutory mandate from Congress. That’s not quite an official legal category, but it’s commonly treated like a specific kind of rule by judges and lawyers.

If a rule is designed to implement a specific part of a law passed by Congress, then the rule has to be in keeping with that law.

And it does not appear that Congress intended for the word “gaming” to be read as only casino games.

‘Solely for gambling’

On the Senate floor in 2010, during discussions about the Dodd-Frank amendments to the CEA, Sen. Blanche Lincoln answered questions from Sen. Dianne Feinstein about the purpose of the special rule, which Lincoln — now a Kalshi lobbyist — is generally credited with writing.

Most notably, she specifically brought up the idea of sports event contracts as something that “should” be banned.

“The commission needs the power to, and should, prevent derivatives contracts that are contrary to the public interest because they exist predominantly to enable gambling through supposed ‘event contracts,’” Lincoln said.

“It would be quite easy to construct an `event contract’ around sporting events such as the Super Bowl, the Kentucky Derby, and Masters golf tournament.

“These types of contracts would not serve any real commercial purpose. Rather, they would be used solely for gambling.”

While judges have differing views on how to take legislative history into account, the apparent congressional intent to include sports contracts under the special rule may be a difficult obstacle to overcome.

“They may have some leeway, but they can’t go against what Congress wanted,” David Aron, special counsel at Lowenstein Sandler, told InGame.

Changing the rule

The whole matter would be a lot easier for the CFTC if the wording of 40.11 was closer to the special rule. The CFTC could have written a rule where the text explicitly states that it operates a two-part test, and can wave through any contracts it likes as long as it believes them to be in the public interest. At that point, the definition of gaming would be irrelevant.

But it didn’t write that rule. And it didn’t change it when sports event contracts were first contemplated either.

“I don’t know why the acting chair [Caroline Pham] didn’t do anything about that because I think she’s written about thinking that the regulation is shoddy,” the commodity futures law expert says. “She did a lot of one-off things, but she never did anything about that.”

The CFTC can make an effort to change the rule now, but it would probably be a slow process.

Again, the ties between rule 40.11 and congressional statute become important.

Because 40.11 is implementation of a law passed by Congress, it carries the force of law and so any changes are expected to go through notice and comment.

The CFTC has put out advanced notice of proposed rulemaking on event contracts, which is likely to be a first step toward changing its rules, possibly including 40.11.

“40.11 is part of why they did that advanced notice of proposed rulemaking,” Aron said.

However, the advanced notice consisted of a series of questions on just about every topic relevant to the regulation of event contracts, so there haven’t yet been any specifics on changing the rule. The CFTC would have to finish collecting comments on the advanced notice, then draft its own new rules, then take comment on those, adjust the rules as needed, send the rules to the Office of Information and Regulatory Affairs, and submit it to the Federal Register. That could take over a year.

Good cause?

There could be another option: attempting to skip notice and comment. But it would be controversial.

President Trump arguably cleared this path for the CFTC, via an executive order signed last year in which the White House instructed federal agencies to remove what it called “unlawful regulations,” typically regulations that the administration argues go beyond what Congress authorized, via the “good cause” exception in the Administrative Procedure Act.

“That exception allows agencies to dispense with notice-and-comment rulemaking when that process would be ‘impracticable, unnecessary, or contrary to the public interest,’” the White House said. “Retaining and enforcing facially unlawful regulations is clearly contrary to the public interest.”

The commodity law expert noted that this could in theory be a path for the CFTC.

“The Administrative Procedure Act typically requires a comment period, but if there’s good cause you don’t need it,” he said. “The memo said if it’s illegal, that’s good cause.”

During oral arguments, Crypto.com’s lawyer Shay Dvoretzky suggested that if read literally as a blanket ban, 40.11 would be illegal because it doesn’t include the public interest test that the special rule implies should exist.

But it would likely be a challenge that any change would come about not in the 60-day period laid out by the executive order, but more than a year later, once the rule became inconvenient. That would not look like much of an “emergency” and may be challenged.

How much does 40.11 really matter?

Of course, there’s no guarantee that 40.11 will ultimately be the defining issue in the lawsuit. It has come up to some degree in other cases, but in no other Kalshi-vs.-state lawsuit has it been so central.

“I don’t think the case rises or falls on 40.11, but maybe it could be critical to this court,” Aron said.

Nelson’s reading of the rule makes sense, especially if you think the literal meaning of the text must take precedent.

But a tougher question may be whether compliance with the rule can be the defining factor in a lawsuit about federal preemption of state laws.

Nelson’s reasoning was that if a prediction market doesn’t comply with CFTC rules, it would be fair to say that it’s “not on the DCM,” and so any preemption of state laws that applies to registered DCMs would not cover the business.

It’s one interpretation, but it’s far from settled. If a DCM violates CFTC rules, does it naturally follow that preemption doesn’t apply?

“I think it doesn’t make sense that a CFTC regulation of what happens on a DCM could mean that if it happens on the DCM, it’s not preempted,” the commodity futures law expert said.

The rule taking center stage in oral arguments doesn’t necessarily mean that it will be the deciding factor in the case itself, Aron noted.

“Sometimes they ask them to focus on specific issues in oral argument because they understand the others pretty well,” he said. “Maybe he’s just incredulous that they’re arguing the other side.”