Robinhood’s share of volume on Kalshi has fallen from almost 60% in September to less than 23% in the first 27 days of March, in a sign that the stock trading giant is losing its status as a kingmaker in the prediction market world.

In an update to the stock market on Monday afternoon, Robinhood revealed that its users had traded 2.6 billion contracts.

With each contract traded being worth one dollar, 2.6 billion contracts traded is $2.6 billion of volume.

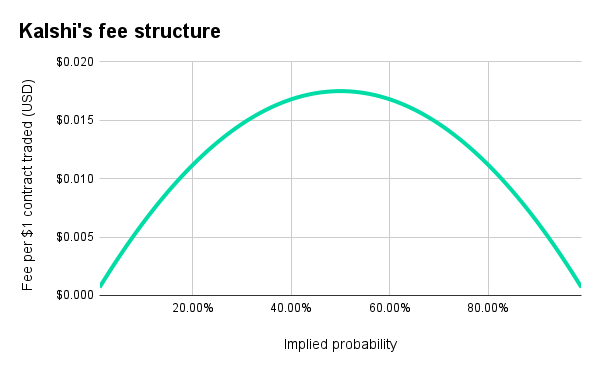

Robinhood charges a flat one-cent fee on every contract, on top of the fees charged by Kalshi, meaning that it made $26 million in fees during those 27 days.

If average volume during the last four days of March was the same as during the first 27, Robinhood’s volume for the month would be just under $3 billion. Even if volume is higher during those four days, it is unlikely to top $3.1 billion.

This means that the business is almost certain to process less prediction market volume in March than it did in January, when it processed $3.4 billion worth of trades. In February, it fell to $2.4 billion.

Volume rose fairly slowly between October, when Robinhood recorded $2.5 billion in volume, through January, and has been lower since.

Much lower share of Kalshi volume

Not only would it put Robinhood on course for a decline from January to March, it would represent a dramatic fall in its share of volume on Kalshi in recent months.

For the first nine months after launching its “predictions hub,” Robinhood was responsible for more than half of volume on Kalshi. In September, its share peaked at 59.4% as Robinhood processed $1.7 billion of Kalshi’s $2.86 billion in volume during the first month of the NFL season.

In late September, Robinhood CEO Vlad Tenev wrote on social media site X, “’Turns Out The Robinhood Of Prediction Markets is … Robinhood.” That post appeared to have come at almost the exact peak of Robinhood’s market share.

By January, that share had clearly fallen. While Robinhood hit a new record in volume with $3.4 billion, that was less than 40% of Kalshi’s volume for the month.

In the first 27 days of March, Kalshi’s volume continued to soar to new highs, while Robinhood’s has failed to grow.

The stock trading app was responsible for just 22.6% of volume on Kalshi from March 1-27. Total Kalshi volume for the 27-day period was $11.49 billion.

Robinhood’s fees being added on top of Kalshi’s mean that Kalshi contracts on Robinhood are always more expensive than the same contracts bought directly through Kalshi. In addition, by charging a flat fee per contract – in comparison to Kalshi’s dynamic pricing that changes depending on the odds – bets on overwhelming favorites or distant longshots come with fees that can represent an extremely large share of the original stake or potential winnings. For example, a bet at 99-cent odds on Robinhood is guaranteed to lose money, and a bet at one-cent odds has an effective vig of more than 100%.

Robinhood also offers ForecastEx contracts

While most event contract purchases facilitated by Robinhood are for contracts on Kalshi, it also offers contracts from ForecastEx.

ForecastEx processed $37.2 million in trading volume in the first 27 days of March. Robinhood likely made up a very large share of this total, but even if all ForecastEx trades were from Robinhood, the totals are low enough to be a rounding error when compared to Robinhood’s total volume.

At times, ForecastEx’s volume for a single day has soared, almost certainly due to Robinhood directing customers towards ForecastEx contracts rather than Kalshi’s. For example, on Jan. 4 – the last Sunday of the NFL regular season – volume on ForecastEx topped $50 million.

There were no particularly high-volume days on ForecastEx during March, suggesting that Robinhood did not direct customers of any of its most popular markets toward ForecastEx during the month.

‘Kalshi Direct’ growing fast

From Kalshi’s perspective, the slowing Robinhood share means that it must be growing in volume either organically or via other distribution channels.

Volume on Kalshi excluding all Robinhood volume in March and April of 2025 was around $200 million. By September, it was $1.2 billion as Robinhood’s event contracts and Kalshi’s non-Robinhood volume grew at similar pace. In January, Kalshi’s growth outpaced Robinhood’s, and Kalshi’s volume excluding all Robinhood contracts topped $6 billion. In the first 27 days of March, that figure reached $8.5 billion.

Kalshi has other non-Robinhood partners that direct customers to the exchange. For example, it also has agreements with daily fantasy sports operator PrizePicks and financial app Plus500.

However, it is likely that much of the growth is from traders using Kalshi’s website or app directly.

Appearing on payments firm Stripe’s Cheeky Pint podcast on March 17, Kalshi CEO Tarek Mansour said the “Kalshi direct” offering was growing much faster than the intermediated business.

“We won’t share numbers, but what we call Kalshi Direct, which is Kalshi.com and the Kalshi app, the consumer business, that has grown,” he said. “That has sort of dramatically outpaced the rest, our other sort of intermediary or broker business. And I think it’s just that the brand has gone mainstream.”

Robinhood falls as parlays rise

Robinhood’s declining share of volume coincides with the rise of parlays on Kalshi.

Parlays have an outsized effect on volume numbers, as most are at long odds and the “maker” side of a parlay is virtually always a professional or institutional market maker. Kalshi counts the amount staked by both the “taker” and the “maker” towards volume, so a $1 parlay at 10% odds would be $10 worth of volume.

Parlays, thanks in part to this effect, have quickly risen to become a large share of trading on Kalshi.

Robinhood was fairly slow to allow users to make parlay bets, first doing so in January — more than three months after Kalshi launched parlays on its own app. By that time, parlays on Kalshi were already contributing tens of millions in volume per day.

However, even if parlays are ignored entirely, Robinhood’s share of Kalshi’s volume is still much lower than it was six months ago. Excluding all parlays from Kalshi’s volume, but counting all Robinhood trades, Robinhood’s share of volume would still be only 27%. If only the “yes” side of parlays are counted for Kalshi, Robinhood’s share would be 26%.

Robinhood’s declining share could be important as the business prepares to launch its own exchange, Rothera. While the stock trading app will not abandon Kalshi when Rothera goes live, it is likely that its main priority will be routing customers to Rothera contracts instead of Kalshi ones.

Were the stock trading app still responsible for more than half of Kalshi’s volume, the loss of Robinhood customers could have been catastrophic for Kalshi. However, with Robinhood now representing less than a quarter of Kalshi volume, the potential loss will likely be much more manageable.

On Robinhood’s side, the built-in customer base for Rothera may be smaller than the stock trading giant expected when it announced plans to buy a designated contract market and offer its own contracts in November. However, operating the exchange itself may allow Robinhood to offer lower fees than it does when offering Kalshi’s contracts. This might encourage a rebound for the business.

Robinhood shares have fallen in 2026

Robinhood, which in Q4 of 2025 made less than 7% of its revenue from event contracts, has seen its shares plunge since early October, due in part to a major cryptocurrency downturn. Its shares fell by 58.2% from their peak in early October to a low of $63.98 Monday, wiping almost $80 billion from its market cap, before rising by more than 5% Tuesday.

While Robinhood is not experiencing the same growth as Kalshi, its business model of directing customers to contracts traded on another exchange, and taking commission on every purchase, may still be lucrative. Overhead costs are low, meaning that a much greater share of Robinhood’s revenue from event contract fees run straight to the bottom line.

Analysis from Sporttrade CEO Alexander Kane and COO David Huffman on their Buy Low Sell High newsletter estimated that almost 95% of Robinhood’s gross revenue from sports event contracts would flow through to gross profit. In contrast, they estimated around 60% of FanDuel’s revenue becomes gross profit.