Last updated: April 27, 2026 | Last verified: April 27, 2026

Peer-to-peer sports betting means you’re trading against other users instead of against a sportsbook or “the house.” That’s the one-sentence version. The longer version is that “P2P sports betting” has become an umbrella term covering everything from CFTC-regulated prediction markets like Kalshi and Polymarket (which now process billions in monthly volume) to sweepstakes-model exchanges like Novig to legacy betting exchanges like Betfair that most Americans have never used.

I’ve had active accounts on PredictIt dating back to 2008, as well on many of the U.S. platforms including Kalshi that took off in the fall of 2024. They share a label, but there are some meaningful differences between them. While they’re generally similar on the surface, underneath, the fee structures, the counterparties, the regulatory frameworks, and the tools available will vary. This page breaks all of that down.

Our Top Prediction Market Apps

If you just want a quick recommendation: Kalshi is the best all-around P2P sports trading platform for most U.S. users right now. Widest market selection, most liquidity on sports, available in 49 states plus DC, and your balance earns 3-4% APY. Polymarket US has lower fees and a ton of potential, if you can get past the waitlist and if the U.S. product eventually resembles the international version. For the full comparison, see our Kalshi vs. Polymarket breakdown.

The P2P sports betting landscape in 2026

The label “peer-to-peer sports betting” now covers at least four distinct models, each with different regulatory status, fee structures, and user experiences. Kalshi and Polymarket dominate the volume, but the field has gotten crowded fast and includes some well-financed, capable operators from the state-regulated sports betting ecosystem.

| Platform Type | Examples | Regulator | Fee Model | U.S. Availability | API Access |

|---|---|---|---|---|---|

| CFTC Prediction Markets | Kalshi, Polymarket, Crypto.com, Robinhood | CFTC (federal) | Maker/taker coefficient (1-7%); varies | Most or all states (18+) | ✅ Full (Kalshi, Polymarket) |

| Sweepstakes Exchanges | Novig, ProphetX | Sweepstakes model (state-level) | 0% (Novig); varies | 38-42 states (21+) | ❌ |

| Sportsbook Prediction Arms | DraftKings Predictions, FanDuel Predicts, Fanatics Markets | CFTC (via partnerships or own DCM) | Flat per-contract or built into spread | Varies by product | ❌ |

| Legacy Betting Exchanges | Betfair, Smarkets, Matchbook | UK/international gambling licenses | 2-5% commission on net winnings | ❌ (not available in U.S.) | ✅ (Betfair) |

So far, the CFTC-regulated prediction markets have largely eaten the lunch of every other P2P model in the U.S. They’re available in more states, to a younger age group (18+ vs. 21+, which is a point of controversy), with deeper liquidity and more market variety. That doesn’t make the other models irrelevant, but it does explain why Kalshi’s weekly trading volume now regularly exceeds $1 billion while most standalone P2P exchanges struggle to match that in a month.

How peer-to-peer sports trading works

Every P2P sports trade has the same basic structure: you’re buying or selling a contract tied to an outcome, and another user is on the other side.

On prediction markets like Kalshi and Polymarket, contracts are priced between $0.01 and $0.99. That price reflects the market’s collective estimate of the probability that the event will occur. If a contract on the Knicks winning tonight trades at $0.62, the market thinks there’s roughly a 62% chance it happens.

💡 A real trade, and the math:

You buy 100 “Yes” contracts on the Knicks at $0.62 each = $62 total cost.

Knicks win: 100 contracts × $1.00 = $100 payout. Your profit: $38 (minus fees).

Knicks lose: contracts expire at $0.00. You lose your $62.

At a sportsbook, this same implied probability would look like roughly -163 on a moneyline. Same bet, different notation, but on the exchange you can sell those contracts at any point before the game ends if the price moves in either direction.

On sweepstakes exchanges like Novig, the on-screen mechanics look more like a traditional sportsbook (American odds, spreads, totals), but the underlying structure is the same: your wager is matched against another user, not the house.

The critical difference from a sportsbook is that you can trade out of your position at any time. Bought those Knicks contracts at $0.62 and they go up 15-2 in the first quarter? The contract price might rise to $0.85. And you could sell for a $0.23 profit per contract without waiting for the final buzzer. That flexibility is closer to trading stock options than placing a bet. You may get cash out offers at traditional sportsbooks, but typically for a dollar value that’s well below the implied probability of the outcome occurring.

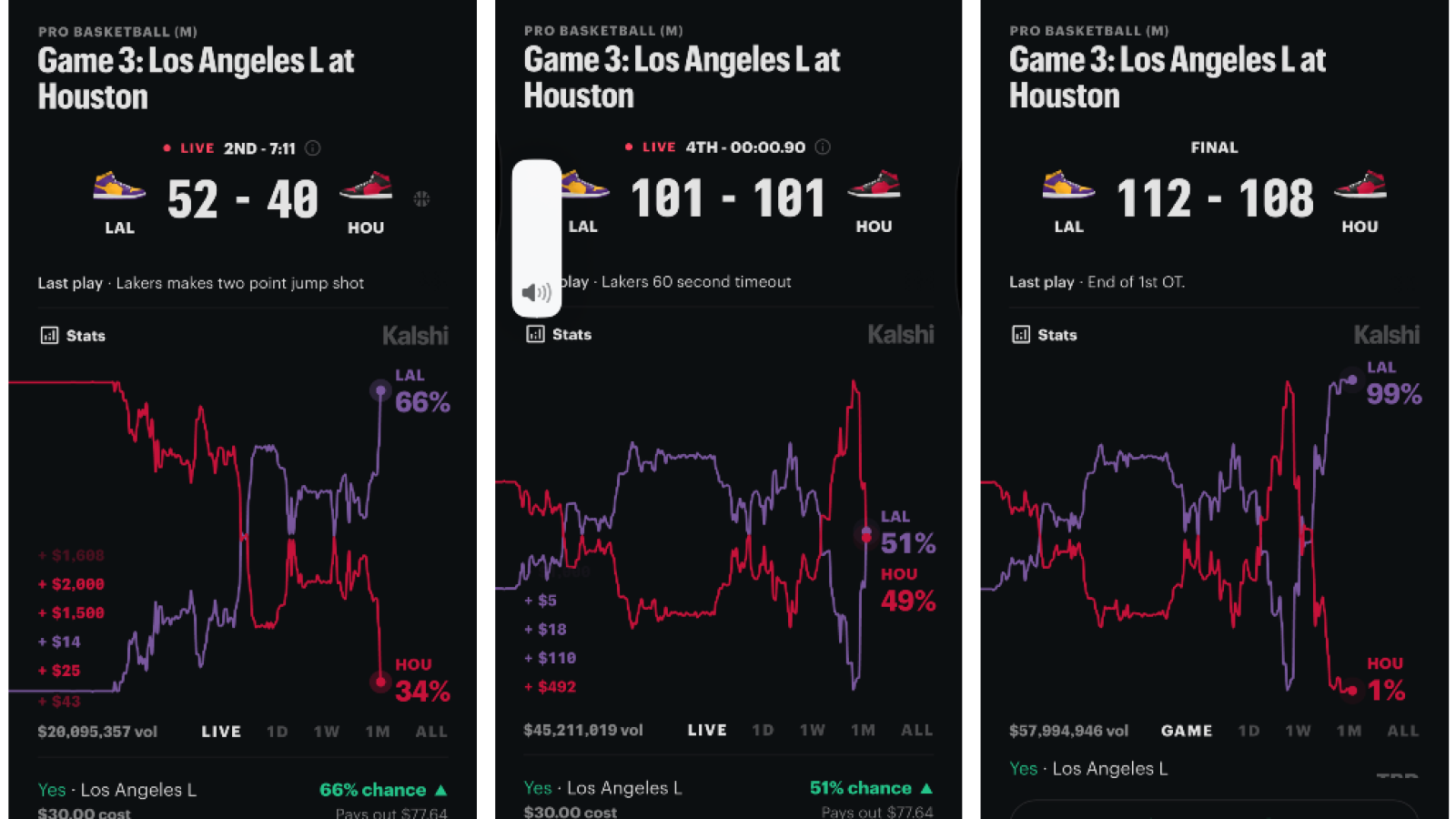

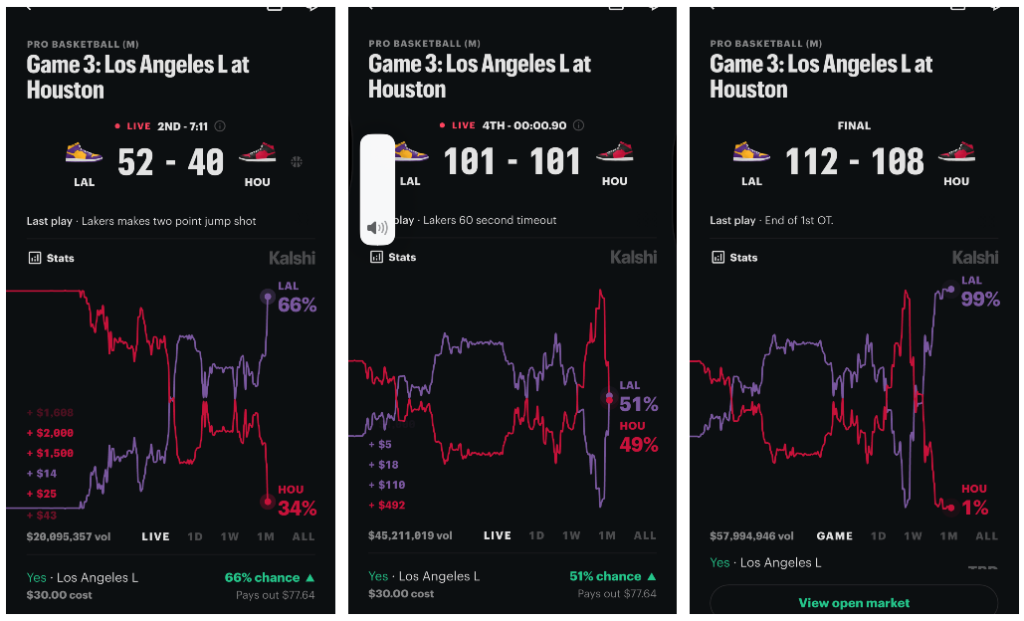

For another example, check out the wild swings that occurred in Game 3 of the Lakers vs. Rockets Round 1 series in April 2026. The Rockets were almost at 99% to win after a LeBron James turnover with about 46 seconds remaining resulting in a 6-point Rockets advantage… only for LeBron heroics to send it to overtime when the market made the overtime outcome roughly a 51/49 contest, favoring the Lakers, who did go on to win by four.

Market orders vs. limit orders

On P2P exchanges, for recreational traders, this is an overlooked but important distinction to understand.

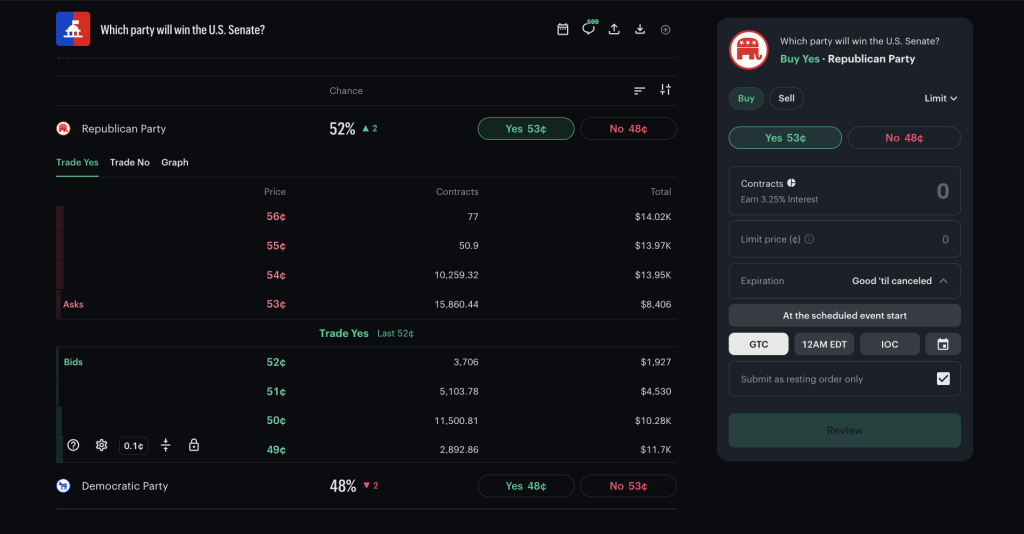

A market order fills immediately at the best available price. You’re “taking” liquidity off the order book. Fast, but you pay taker fees and accept whatever price is available.

A limit order lets you name your price. It sits on the order book until someone takes the other side. You’re “making” liquidity, and you pay lower fees (or no fees, or even earn a rebate). The trade-off is that your order might not fill at all if no one wants the other side at your price.

When I first started trading on prediction markets, I hit “buy” at market price on everything. Once I figured out limit orders, my effective cost per trade dropped by about 60%. If you take one thing from this page, let it be this: learn to use limit orders.

P2P trading vs. traditional sportsbooks

You’ll see “peer-to-peer exchange,” “betting exchange,” and “prediction market” used almost interchangeably, and the lines between them are blurring fast. The structural differences (contract pricing vs. American odds, maker/taker fees vs. commission on winnings, CFTC regulation vs. state gambling licenses) are real, but from a user’s perspective, the experience is converging. You pick a side, another user takes the opposite side, and the platform matches you.

Kalshi now displays American odds as an option. Novig calls itself a “prediction exchange.” FanDuel Predicts uses the phrase “peer-to-peer” in its marketing. The wrapper varies; the underlying trade is the same.

The meaningful divide is between all of these platforms and a traditional sportsbook. That’s where the differences actually affect your wallet.

| Traditional Sportsbook | P2P / Prediction Market | |

|---|---|---|

| Who sets the price? | The house (bookmaker) | Other users, via supply and demand |

| Who’s on the other side? | The sportsbook | Another user (often an institutional market maker) |

| Can you exit early? | Sometimes (cash out, where offered) | Yes, sell anytime before resolution |

| How you pay | Built into the odds (vig/juice, ~4.5-5%) | Per-contract fees (0-7%) or commission on winnings |

| Non-sports markets? | No | Yes (politics, economics, weather, culture) |

| U.S. regulator | State gaming commissions | CFTC (federal) *or* sweepstakes model (Novig, ProphetX) |

| Minimum age | 21+ (most states) | 18+ (CFTC platforms) or 21+ (sweepstakes) |

| Balance earns interest? | No | Kalshi: ~3-4% APY; others: no |

The practical takeaway: If you live in a state with legal sports betting and you’re happy with DraftKings or FanDuel, or like getting those “odds boosts” promos, a sportsbook may be perfectly fine. If you want lower fees, the ability to exit positions anytime, access to non-sports markets, or you live in a state without legal sportsbooks, P2P platforms are worth your time. For deeper reading, see our prediction market vs. sportsbook breakdown.

Liquidity matters

Every P2P platform lives and dies on liquidity. If nobody is on the other side of your trade, the platform is useless regardless of how low the fees are or how clean the app looks.

Liquidity means there are enough buyers and sellers posting competitive prices that you can enter and exit positions quickly without moving the price against yourself. On a sportsbook, liquidity is never your problem; the house offers you a price, and you book it or you don’t. On a P2P exchange, you need someone to take the other side, and if the market is thin, you’ll either wait, or accept a worse price.

This is why nationally available platforms are powerful at scale. Kalshi’s sports markets regularly have tight spreads on NFL, NBA, and MLB games because millions of users are trading in the same pool. A state-restricted P2P exchange with 50,000 users simply cannot match that depth. During the 2026 NBA playoffs I watched Kalshi’s top markets processing hundreds if not thousands of contracts per minute.

⚠️ Before you trade: Always check the order book depth (see above) before placing a trade on any P2P platform. If the spread (gap between the best buy and sell prices) is wider than 3-4 cents on a prediction market, or wider than 10-15 cents of juice on a traditional exchange, the market is too thin and you’re overpaying to get in. Popular markets (NFL primetime, major elections) are usually fine. Niche markets and lower-league sports can be brutal.

Maker/taker fees and liquidity incentives

Fee structures across P2P platforms are a bit messy. Every platform calculates costs differently, which makes apples-to-apples comparisons harder than it should be. I’ve traded on all of the major platforms, and the table below is my best attempt at a fair breakdown at present.

| Platform | Taker Fee | Maker Fee / Rebate | Liquidity Incentives |

|---|---|---|---|

| Kalshi | 7% coefficient (max ~1.75¢/contract at $0.50) | 1.75% coefficient (many markets: $0) | Volume Incentive Program (up to $0.005/contract); Liquidity Incentive Program ($10-$1,000/day for resting orders) |

| Polymarket US | 5% coefficient (max ~$1.25/100 contracts at $0.50) | 1.25% maker rebate (you get paid) | $5M+ monthly liquidity rewards across sports/esports markets; anyone can sponsor rewards on any market |

| Crypto.com | ~2-4% per contract (exchange + technology fees) | Varies | None publicly documented |

| Robinhood | $0.01 per contract | $0.01 per contract | None |

| Novig | 0% (no vig, no commission) | 0% | None |

| Traditional Sportsbook | Built into odds (vig/juice, ~4.5-5%) | N/A | N/A (daily promos instead) |

Novig’s zero-fee model looks best on paper, but remember the liquidity trade-off: a 0% fee means nothing if the market is so thin that the spread eats your edge. Kalshi and Polymarket charge real fees but offer dramatically deeper liquidity on popular markets, which usually results in tighter effective pricing despite the posted fee.

Liquidity rewards: getting paid to provide depth

This is something no sportsbook will ever offer you, and it’s one of the most underappreciated features of P2P trading.

Kalshi runs two incentive programs (both active through September 1, 2026). The Volume Incentive Program is a cashback system: trade in eligible markets during active reward periods and earn a share of the reward pool based on your percentage of total volume, capped at $0.005 per contract. The Liquidity Incentive Program rewards users who place resting orders at competitive prices, with daily payouts ranging from $10 to $1,000 depending on the market and your contribution. You don’t need to opt in; Kalshi tracks eligibility automatically. Kalshi also launched a Sportsbook Hedging Rebate Program in February 2026, specifically designed to attract traditional sportsbooks to hedge their liabilities on Kalshi’s order book, which has the side effect of deepening liquidity for retail users.

Polymarket distributes over $5 million per month in liquidity incentives across sports and esports markets. The reward formula (inspired by the dYdX protocol) scores your resting limit orders based on how close they are to the midpoint, how much size you’re providing, and whether you’re quoting both sides of the market. As of February 2026, Polymarket also opened liquidity reward sponsorship to all users: anyone can attach incentives to any market to attract tighter quotes. That’s a structural shift. A hedge fund that wants to make a large trade on a thin market can now pay to bootstrap the liquidity it needs.

🔑 Bottom Line: On a sportsbook, you pay the vig and that money goes to the house. On prediction markets, a portion of what takers pay goes directly to makers as rebates and incentive rewards. If you learn to use limit orders and provide liquidity in active markets, you can offset (or in some cases exceed) your trading costs. This is genuinely unique to the P2P model.

RFQ: Request for Quote, explained

If you’ve ever traded options or foreign exchange, you’ve seen Request for Quote systems. If you’re coming from sports betting, this will be new.

Kalshi’s and ProphetX’s RFQ system (among others) lets you solicit private quotes from market makers when you want to execute a “combo” (parlay) or a large trade without eating through the visible order book. Instead of placing a market order that moves the price against you as it fills through multiple price levels, you send out a quote request specifying the combo/market and your desired contract size. Market makers respond with private bids. You pick the best one, accept it, and the market maker confirms within 30 seconds. The trade executes at the quoted price.

RFQs are available on any Kalshi market, including and maybe especially for combo (parlay) markets where all sorts of permutations might exist. They’re accessible via REST API, FIX protocol, and WebSocket. For combo markets, which Kalshi classifies as “High Volatility Markets,” the timing windows are shorter.

Most retail users will never need to touch the RFQ system directly. But it matters for two reasons. First, it attracts institutional market-making firms to the platform, which deepens the order book that you trade against. Second, if you’re trading with meaningful size (say, $500+ on a single market), RFQ can get you a better fill than a market order.

Polymarket does not currently offer a comparable RFQ system for retail users. Its liquidity infrastructure relies on the incentive programs and organic market making described above.

API access and algorithmic trading

This is where P2P sports trading diverges most dramatically from anything in the sportsbook world. Both Kalshi and Polymarket offer full programmatic APIs that let users build trading bots, pull real-time market data, automate order execution, and run quantitative strategies.

Kalshi’s API is a tiered system with 86+ endpoints covering portfolio management, order operations, market data, exchange status, historical data, and the RFQ system described above. Authentication uses RSA key pairs. Real-time data streams via WebSocket include ticker updates, trade feeds, order book deltas, fill notifications, and RFQ communications. Kalshi offers a demo environment for testing before going live.

Polymarket’s API is organized into three services: the Gamma API (market metadata and discovery), the CLOB API (central limit order book for executing trades), and the Data API (positions, trade history, user-specific data). As of February 2026, these APIs are fully public. The CLOB API supports order placement, cancellation, and real-time WebSocket streaming. Polymarket’s API documentation also exposes the liquidity reward formulas, which means algorithmic liquidity providers can optimize their quoting strategies programmatically.

DraftKings Predictions, FanDuel Predicts, Robinhood, Crypto.com, and Novig do not offer comparable public trading APIs as of right now.

💡 What this means for regular users:

You don’t need to write code to trade on these platforms. But you should know that API access exists, because it explains who’s on the other side of your trades. When you place a market order on a popular NFL contract, your counterparty is often not another casual fan. It’s a trading firm running quantitative models, executing thousands of orders per day through the API. That’s not necessarily bad (they provide the liquidity that makes your trades execute quickly), but it means you’re competing against sophisticated participants. Go in with clear eyes. For more on this dynamic, see the institutional traders section of our Kalshi bonus page.

Who you’re actually trading against

P2P platforms market themselves as user-vs.-user exchanges. That’s technically true. It’s also incomplete.

On Kalshi, major institutional players like Susquehanna International Group (SIG), one of the largest quantitative trading firms in the world, operate as market makers. They quote prices on both sides of contracts and profit from the spread. Kalshi also has affiliated for-profit market-making arms that participate on the exchange. The Sportsbook Hedging Rebate Program is explicitly designed to bring sportsbook operators onto the platform as traders, adding another layer of professional counterparty flow.

On Polymarket, the $5M+ monthly liquidity incentive pool attracts professional market makers who deploy algorithmic strategies via the public API. The permissionless liquidity sponsorship system means that hedge funds, institutions, and well-capitalized individuals can bootstrap depth in any market they want to trade.

Novig and ProphetX have less institutional participation, which is both a feature and a limitation. You’re more likely to be trading against another retail user, but the trade-off is thinner liquidity and wider spreads.

None of this means the P2P model is broken. Competition from market makers generally tightens spreads and improves prices for retail users. But the dynamic is closer to a retail options trader executing against a professional market-making desk than it is to two friends making a side bet. A George Washington University research paper found that the expected return on the average Kalshi contract after fees was negative 20%, not dissimilar from the house edge on many casino games. If you’re trading casually with small positions and treating it as entertainment, institutional counterparties are mostly a background feature. If you’re trying to generate consistent profits, understand that the competition is fierce.

Where P2P sports betting is legal

The litigation picture is changing frequently, but the general framework is straightforward for now.

CFTC-regulated prediction markets (Kalshi, Polymarket, Crypto.com, FanDuel Predicts, Robinhood) operate under federal oversight as Designated Contract Markets. This means they can legally offer event contracts in most or all U.S. states, regardless of whether those states have legalized sports betting. Kalshi is currently available in 49 states plus DC; only Nevada has issued a temporary restraining order (March 2026). Multiple other states have active litigation but Kalshi remains operational in all of them. Polymarket is in all 50 states but still in invite-only beta. The minimum age is 18+ on CFTC platforms.

Sweepstakes exchanges (Novig, ProphetX) use a sweepstakes legal framework that allows them to operate in roughly 38-42 states depending on the platform, with a 21+ age requirement.

The jurisdictional battle is far from settled. Several states argue that sports event contracts are functionally indistinguishable from sports bets and should be subject to state gambling laws. Federal courts are deeply split on the question. For the full breakdown, see our coverage of the states vs. federal prediction markets battle and the state-by-state guide on the Kalshi bonus page.

Sports and markets available

Sports: NFL, NBA, MLB, NHL, NCAAF, NCAAB, WNBA, UFC/MMA, PGA Tour, ATP/WTA tennis, soccer (MLS, EPL, La Liga, Bundesliga, Serie A, Champions League), boxing, golf, motorsports, esports, chess, and cricket. Market types include moneylines, spreads, totals, player props, futures, and combo/parlay contracts (Kalshi calls these “Combos”). Live in-game trading is available on Kalshi for most major sports.

Beyond sports: This is where prediction markets flourish, and perhaps is the best use case. With markets on politics (elections, legislation, government actions), economics (inflation, interest rates, GDP, employment data), crypto (Bitcoin and Ethereum price targets), climate and weather, companies (CEO changes, earnings, layoffs), pop culture (awards shows, box office), and world affairs. For more on available markets, see our best prediction market sites roundup or our prediction markets explainer.

💰 Banking and deposits

Deposit and withdrawal options vary significantly across P2P platforms. Here’s the short version for the major players:

| Platform | Deposit Methods | Crypto? | Interest on Balance |

|---|---|---|---|

| Kalshi | Debit card, ACH, wire, USDC | ✅ USDC | ~3-4% APY (including open positions) |

| Polymarket (U.S.) | Credit/debit card, bank transfer, USDC | ✅ USDC | 4% holding reward on select markets |

| Crypto.com | Apple Pay, Google Pay, debit card, wire, ACH, crypto conversion | ✅ Convert holdings to USD | Via cash sweep program |

| Novig | Debit card, ACH | ❌ | No |

| DraftKings Predictions | Standard DraftKings methods (bank, card, PayPal) | ❌ | No |

Kalshi’s interest on deposits (including funds in open positions) is a genuine differentiator. If you’re maintaining a $1,000 balance on the platform, that’s $30-40 per year in interest income that no sportsbook and no other major P2P exchange currently matches. It won’t make you rich, but it quietly offsets trading costs over time.

Polymarket’s U.S. platform does not require a crypto wallet. You can fund your account with a regular debit card. The international version is crypto-only (USDC on Polygon), but if you’re a U.S. resident, the U.S. version is the only legal way to trade.

🛡️ Responsible gambling

P2P sports trading carries real financial risk. Contracts can and do expire worthless. The ability to trade in and out of positions in real time can create a compulsion loop that’s harder to step away from than a traditional locked-in bet.

Responsible gambling tools vary across platforms. Kalshi integrated IC360’s SelfExclude tool in April 2026, making it the first prediction market to offer cross-platform voluntary self-exclusion. Polymarket’s responsible gambling features remain limited, and this is a genuine gap. Sportsbooks are further ahead on this, with deposit limits, loss limits, cooling-off periods, and self-exclusion programs mandated by state regulators.

If your trading activity is becoming a problem, support is available.

🛡️ Responsible Gambling Resources: National Council on Problem Gambling: ncpgambling.org | Call or text 1-800-GAMBLER (1-800-426-2537) | Available 24/7, confidential.

Frequently asked questions

What’s the difference between a prediction market and a P2P exchange?

Mostly branding. Both involve trading against other users rather than a house. Prediction markets (Kalshi, Polymarket) use $0.01-$0.99 contract pricing and are federally regulated by the CFTC. Traditional P2P exchanges (Novig, ProphetX) often use American odds and operate under sweepstakes or state-level frameworks. The mechanics under the hood are similar.

Do I need to know how to code to use the API?

Yes, the trading APIs on Kalshi and Polymarket require programming knowledge (Python, JavaScript, Rust, etc.). Most retail users trade through the app or website and never touch the API. The API’s main impact on casual users is indirect: it attracts institutional market makers whose activity tightens spreads and improves the prices you see on-screen.

Can I actually make money providing liquidity?

It’s possible but not easy. Kalshi’s Volume Incentive Program caps rewards at $0.005 per contract, and Polymarket’s liquidity rewards require placing competitive limit orders consistently. Professional market makers earn from this. A retail user with a small balance and limited time is unlikely to generate meaningful income from liquidity provision alone, but the maker fee savings from using limit orders instead of market orders are real and add up over hundreds of trades.

Which P2P platform should I start with?

Probably Kalshi. It’s available in 49 states, has the widest sports market selection, requires only a $1 minimum deposit, and the $10 welcome bonus (code INGAMEPRO) gives you enough to experiment. Polymarket is on the ascent too if you can get past the waitlist (code INGAME bypasses it). Having accounts on both is ideal for getting the best price on any given trade.

Related InGame coverage

- What Are Prediction Markets? How Do They Work?

- Prediction Markets Explained: How Prediction Trading Works in Sports

- Prediction Market vs. Sportsbook: What’s the Difference?

- Best Prediction Market Sites for Sports Betting in 2026

- Kalshi vs. Polymarket: Which Prediction Market Is Better?

- U.S. Prediction Markets: A Modern Timeline

- States Rights vs. Federalism: Can Prediction Markets Be Kept at Bay?