Last updated: April 28, 2026 | Last verified: April 28, 2026

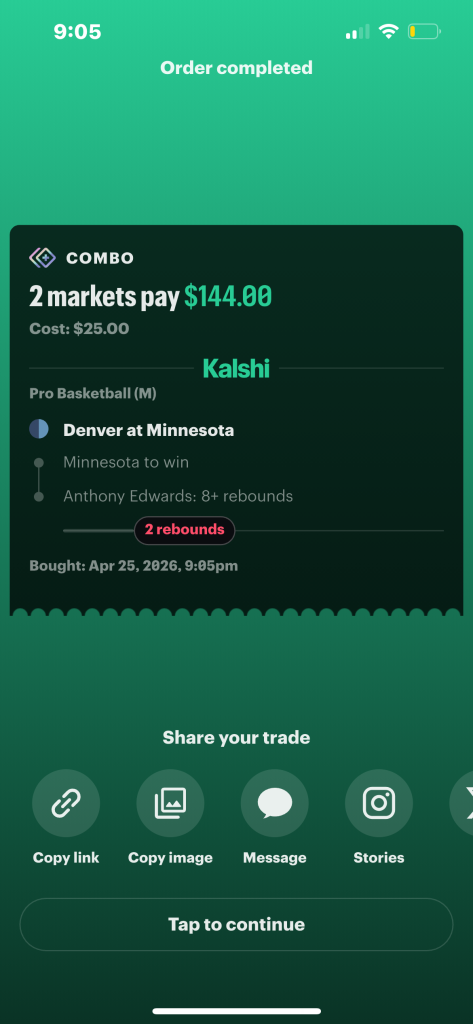

I placed a live two-leg combo on Kalshi last Saturday night: Minnesota to win Game 4 against Denver, and Anthony Edwards to grab 8+ rebounds. Cost me $25 for a potential $144 payout, roughly 5.76x. The pregame spread had the contest roughly a pick’em, and the Nuggets led 40-36 at the time of the trade in the second quarter. Edwards already had 2 rebounds at the time of the trade and was looking active on the glass and had averaged 8 per game so far in the series.

Then Edwards hyperextended his left knee contesting a layup in the second quarter and was wheeled out of Target Center. Not great. Minnesota still won 112-96 behind Ayo Dosunmu’s 43-point eruption off the bench, but that didn’t matter for my combo. The Edwards leg settled short of the 8-rebound threshold, and the whole thing paid out zero. Twenty-five bucks, gone to the combo gods.

That trade, in one screenshot, captures much of what you need to know about prediction market parlays: the structural appeal (no compounding house vig, a real 5.76x on a two-legger), the correlation opportunity (same-game legs that reinforce each other), and the reality that all legs must hit. Injury risk, which sportsbook parlays and prediction market combos share equally, can wipe you out just the same. (Although, some sportsbooks do offer forms of “injury protection” in some cases as a promotional item.)

This guide covers how prediction market combos actually work (the RFQ mechanism that prices them), which platforms offer them, the math on when they beat sportsbook parlays and when they don’t, and the institutional counterparty dynamic that every combo trader should understand.

🎯 What are prediction market parlays?

A prediction market parlay (called a “Combo” on Kalshi and Fanatics Markets) bundles two or more event contracts into a single position. All legs must resolve “Yes” for the combo to pay out $1.00 per contract. If any single leg resolves “No,” the entire combo pays $0.

The concept is identical to a traditional sportsbook parlay. The mechanics are not.

On a sportsbook, the house sets parlay odds by multiplying the individual implied probabilities together and then layering a vig on top. Each additional leg compounds that vig. A three-leg sportsbook parlay typically carries 10-13% effective vig. Four legs can push past 15%. The more legs you add, the worse the deal gets relative to fair/true odds.

On a prediction market, nobody sets odds, exactly. You submit a combo, and institutional market makers compete to price the other side. The pricing mechanism is called RFQ (Request for Quote), and understanding how it works is the key to understanding whether combos are a good deal for you.

⚙️ How combos work: the RFQ system

The RFQ (Request for Quote) system is what makes prediction market parlays structurally different from sportsbook parlays. It’s also the part that almost nobody explains clearly.

Here’s the step by step:

- You pick your legs. Select two or more contracts from eligible markets. On Kalshi, that’s currently NFL, NBA, and “Mention” markets (and on mobile-only, for now). On Fanatics Markets, it’s broader: basketball, baseball, hockey, soccer, football, boxing, MMA, and tennis.

- You submit the combo as an RFQ. This is not a regular order. You’re not buying from a visible order book. You’re requesting a price from the market.

- Market makers receive the RFQ and respond with quotes. Multiple institutional participants evaluate your combo, assess the correlation between legs, factor in their risk models, and each submit a private bid. They can see your combo request but not each other’s quotes.

- Kalshi shows you the best available price. This happens in seconds. You see a combo price (say, $0.11 per contract) and decide whether to take it.

- You accept or reject. If you accept, the trade fills. If you reject, nothing happens. Quotes are live and may change between viewing and execution.

The critical difference from a sportsbook: no single entity sets the price. Market makers compete against each other to fill your RFQ. In theory, this competition drives the price toward fair value. In practice, the market makers are sophisticated institutional trading firms with proprietary models, and they’re not offering you a fair coin flip.

⚠️ Important: On Kalshi, retail users can only be takers on combos, not makers. You cannot set your own combo price and wait for someone to fill it. You submit an RFQ and accept or reject whatever comes back. This is structurally closer to a sportsbook model (you take the offered odds) than to the regular Kalshi exchange (where you can post limit orders). Fanatics Markets operates similarly through Crypto.com’s infrastructure.

📊 The math behind my Wolves combo (and a 3-leg hypothetical)

Let’s break down the real trade from the opener. My two-leg combo was:

- Minnesota to win (the Wolves were slight home underdogs and trailing by a few at the time; this contract probably priced around $0.45-0.47)

- Anthony Edwards 8+ rebounds (a player prop stretch; Edwards averaged ~5.5 RPG regular season and 8 in the series, so this likely priced around $0.33-$0.38)

The theoretical combo price: Multiply the individual probabilities. Using midpoint estimates: 0.48 x 0.36 = 0.173, or about $0.17 per contract. My actual RFQ quote came back at approximately $0.174 per contract ($25 cost / 144 contracts). That’s pretty close to the mathematical product, meaning the market maker applied almost no spread on this particular combo. That won’t always happen, but on a liquid NBA playoff game with a simple two-legger, the pricing was competitive.

The payout math: $25 invested, $144 potential payout. That’s 5.76x, or roughly +476 in sportsbook odds. A traditional two-leg parlay at those same individual probabilities would price around +400 to +450 after the book’s vig. The combo offered a better deal by about 0.5x to 1x, which is the structural no-compounding-vig advantage in action.

Now scale it to three legs. Say I’d added a third leg: Denver/Minnesota Over 215.5 (pricing around $0.48). The theoretical combo price drops to 0.48 x 0.36 x 0.48 = ~$0.083 per contract, or about 12x potential return. The equivalent sportsbook three-leg parlay would be around +900 to +950 (10-10.5x) after compounding vig. The gap widens with each leg because the sportsbook’s vig compounds while the market maker’s spread stays relatively flat.

| Metric | Kalshi Combo (RFQ) | Sportsbook Parlay |

|---|---|---|

| Cost per unit | ~$0.174/contract ($25 total) | $25 wager |

| Potential payout | $144 (144 contracts x $1.00) | ~$125-$137 (+400 to +450) |

| Potential return | 5.76x (+476) | ~5.0-5.5x (+400 to +450) |

| Embedded vig/spread | Market maker spread (~minimal on this trade) | Compounding vig (~8-10% on 2 legs) |

| Can exit early? | Yes (sell at market price) | Cash-out if offered (not guaranteed) |

| Who sets the price? | Competing market makers via RFQ | The sportsbook (house) |

The combo offered roughly 0.5x to 1x better return than a sportsbook parlay on the same legs. It also wins on structural transparency: I could see the individual leg prices and verify that the RFQ quote was fair (in this case, almost exactly at the mathematical product). On a sportsbook, the vig is opaque and baked into the multiplier. (That said, most sportsbooks let you see individual leg prices in their SGP builder, so you can do a rough comparison there too.)

But there’s a catch. The combo price isn’t always this competitive. If the market maker assesses positive correlation between your legs (e.g., a team winning AND a player on that team hitting a prop in the same game), the RFQ quote might price above the simple multiplication of individual probabilities. Correlation cuts both ways. In my Wolves combo, the correlation thesis (Minnesota wins a physical game, Edwards is active on the boards) was the whole point of the trade. The market maker priced it almost flat, which suggests they either didn’t model the correlation strongly or the competitive RFQ process drove the price down.

🔄 Prediction market parlays vs. sportsbook parlays

The structural comparison favors prediction markets over sportsbooks in most scenarios. But “most” is not “all.”

Where combos win: Two- and three-leg combos on liquid markets (NFL moneylines, NBA spreads) typically offer better effective odds than equivalent sportsbook parlays. The absence of compounding vig is a genuine structural advantage. On a sportsbook, the effective vig on a 3-leg parlay runs about 10-13%. On Kalshi’s RFQ system, the market maker’s spread is more like 2-5% depending on liquidity and correlation. That gap is real money.

Where combos are roughly equal: Same-game parlays (SGPs) on sportsbooks are notoriously overpriced because books aggressively model correlation between legs (think: Joe Burrow 300+ passing and Ja’Marr Chase 100+ receiving). Market makers on Kalshi may price SGP-equivalent combos more fairly, but the liquidity is thinner and the spread can widen to offset any advantage.

Where sportsbooks might actually be competitive: 4+ leg longshots on uncorrelated events. As you add legs, Kalshi’s RFQ liquidity thins significantly. Market makers widen their spread to compensate for the increased risk and modeling complexity. On a 5-leg parlay of uncorrelated events, a sportsbook’s compounding vig and a market maker’s wide RFQ spread can end up in roughly the same neighborhood. I’ve seen RFQ quotes on 4-leg combos that were actually worse than the corresponding sportsbook parlay. Not common, but it happens.

💡 Rule of thumb: Combos shine brightest on 2-3 leg positions in liquid markets. Beyond 3-4 legs, always compare the RFQ quote against the mathematical product of individual contract prices. If the combo price is significantly above that product, the market maker’s spread has eaten your structural advantage, and the sportsbook might actually be a better deal.

📱 Which platforms offer combos?

Combo availability is expanding fast but remains unevenly distributed. Kalshi pioneered the product in late 2025. Fanatics Markets followed in April 2026 with a broader sports catalog. Several other platforms are either missing the feature entirely or haven’t publicly committed to a timeline.

| Platform | Combos Available? | Eligible Sports | Max Legs | Pricing Model |

|---|---|---|---|---|

| Kalshi | Yes (late 2025) | NFL, NBA, Mentions | No hard cap (liquidity thins past 3-4) | RFQ (institutional market makers) |

| Fanatics Markets | Yes (April 2026) | Basketball, baseball, hockey, soccer, football, boxing, MMA, tennis | Up to 4 | Via Crypto.com infrastructure |

| Underdog Predict | Yes | NFL, NBA, MLB, college football | Varies | Via Crypto.com infrastructure |

| Polymarket | Not yet | N/A | N/A | N/A |

| Robinhood | No | N/A | N/A | N/A |

| DraftKings / FanDuel / ForecastEx / PrizePicks | No | N/A | N/A | N/A |

Kalshi has the deepest combo infrastructure (the RFQ system is purpose-built for this), but the narrowest sport coverage. Fanatics Markets has the widest sport selection for combos, but caps you at four legs and routes through Crypto.com’s exchange. If you want a multi-sport combo touching boxing and tennis, Fanatics is your only option right now.

Polymarket does not offer combos on its U.S. regulated exchange. Despite what you might read elsewhere online, Robinhood does not offer combos either. Both may add the feature eventually, but as of late April 2026 neither has announced a timeline.

💰 The fee problem on cheap contracts

This is where the original promise of combos gets complicated. Combo contracts are cheap by design. A 3-leg combo might cost $0.08 to $0.15 per contract. And prediction market fees, even small ones, represent a huge percentage of that cost basis.

Consider a $0.10 combo contract on a platform with a $0.02 flat fee. You’re paying $0.12 for a contract worth $0.10. That’s a 20% fee load before the outcome is even determined. If the combo wins, you collect $1.00 on a $0.12 outlay (8.3x). If it had been priced better at $0.10 with no fee, that’s 10x. The fee ate 17% of your potential return.

Now consider the same $0.10 combo on Kalshi with its variable fee structure (7% coefficient). At a $0.10 contract price, the taker fee is approximately $0.0063 per contract. Your all-in cost is $0.1063, and your effective return on a win is 9.4x. The variable fee barely dents the economics at this price point. That’s the advantage of probability-weighted fees on cheap contracts.

⚠️ Watch Out: Flat per-contract fees on platforms like Robinhood ($0.02) or DraftKings ($0.02) make combo-style trading especially expensive. Even if those platforms add combos in the future, the flat fee structure would make longshot combos significantly worse deals than on Kalshi. This is the single biggest reason fee structure matters for parlay-style trading.

🐻 The institutional counterparty matter

So, this may be the section most combo traders don’t want to hear.

When you submit a combo on Kalshi, the person on the other side of your trade is not another casual fan. It’s an institutional market-making firm with proprietary pricing models, access to Kalshi’s back-end RFQ infrastructure, and the capital to take the other side of thousands of combos per day. Research from University College Dublin found that retail takers on Kalshi’s RFQ combo system lose more often than not, with the institutional market makers consistently earning money from the other side.

This shouldn’t be shocking. It’s the same dynamic as a retail options trader executing against a professional market-making desk at the CBOE. The market maker has better models, faster data, and more capital. They’re not offering you a charitable price.

One former Kalshi employee (Adhi Rajaprabhakaran), who now publishes an industry newsletter, compared the dynamic to a brown bear devouring fish in an Alaskan river. Retail combo users, in his framing, are the fish. Kalshi’s own affiliated market-making arms participate in the exchange, and while this is disclosed, it raises structural questions about whether the exchange functions as a truly neutral intermediary on combo trades.

None of this means combos are a bad product. The structural advantage over sportsbook parlays (no compounding vig, competing market makers, ability to exit early) is real. But the structural advantage doesn’t automatically translate into a trader advantage. You’ve eliminated one source of edge erosion (the house vig) and introduced another (an institutional counterparty who may price the combo more accurately than you can).

💡 Bottom Line: If you’re trading combos casually with small positions for entertainment, the institutional counterparty is mostly a background feature that provides you with liquidity and competitive-ish pricing. If you’re trying to generate consistent profits from combo trading, understand that you’re competing against some of the most sophisticated trading operations in finance. The combo is the product. You might be the customer.

📋 How combos settle

Combo settlement is straightforward in the normal case: if all legs resolve “Yes,” the combo pays $1.00 per contract. If any leg resolves “No,” the combo pays $0. Settlement typically occurs within 1 to 12 hours after the last underlying position resolves.

The edge case to know about is scalar settlement. If a player in one of your combo legs doesn’t play (DNP), that leg may settle at a value between $0 and $1 rather than a binary yes/no. A blue arrow icon on Kalshi indicates scalar settlement. Your combo payout then equals the product of all leg values. So if two legs settle at $1.00 and one settles at $0.70 (due to a DNP rule), your combo pays $0.70 per contract. Not $0, but not the full $1.00 either.

This is different from a sportsbook, where a voided leg in a parlay typically removes that leg and recalculates the payout at reduced odds. On Kalshi, the leg doesn’t get removed. It settles at a fractional value based on the market’s specific rules. Read the settlement rules for every leg in your combo before placing the trade.

📋 Tips for combo trading

- Always compare the combo price to the product of individual leg prices. Multiply the individual contract prices together. If the RFQ quote is more than 10-15% above that number, the market maker’s spread is eating your advantage. Reject the RFQ and consider buying the legs individually.

- Stick to 2-3 legs. Liquidity thins significantly beyond 3-4 legs on Kalshi. The more legs you add, the wider the market maker’s spread. The pricing increasingly favors the institutional counterparty.

- Look for correlated legs. Combos are most interesting when the legs are positively correlated (e.g., a team winning AND the team total hitting over in the same game). If you believe in the correlation more strongly than the market maker’s model does, the combo price may undervalue your edge.

- Use the exit option. Unlike sportsbook parlays, Kalshi combos are tradeable. If two of your three legs have already hit and the last game is trending your way, you can sell the combo at the current market price and lock in profit before the final leg resolves. This is a structural advantage that most combo traders underuse.

- Factor in fees on the total position, not per contract. A $0.02 flat fee on a $0.05 combo contract is a 40% cost load. On Kalshi’s variable fee, the same contract incurs a ~$0.003 fee (6%). The platform you trade on changes the math dramatically on cheap contracts.

- Check settlement rules for every leg. Scalar settlement (DNPs, partial outcomes) can reduce your payout without zeroing it out entirely. Know the rules before you trade.

Frequently asked questions

Are prediction market parlays legal?

Yes, on CFTC-regulated platforms like Kalshi and exchanges operated by Crypto.com (which powers Fanatics Markets and Underdog Predict). Kalshi self-certified its first combo contracts with the CFTC in 2025. Some states have challenged the legality of sports event contracts generally, but these challenges target the contract type rather than the combo feature specifically.

Can I exit a combo position early?

On Kalshi, yes. Combos are tradeable positions. You can sell your combo at the current market price at any time before the final leg resolves. This is a significant advantage over sportsbook parlays, which typically lock you in until all legs settle (with cash-out options that are inconsistent and often unfavorable). On Fanatics Markets, early exit options may be more limited depending on market conditions.

What happens if a player in my combo doesn’t play?

On Kalshi, the affected leg settles at a scalar value between $0 and $1 based on that market’s specific rules. Your combo payout is the product of all leg values. This means a DNP reduces your payout rather than voiding the leg entirely, which is different from most sportsbooks where a voided leg is simply removed from the parlay.

How many legs can I add to a combo?

Kalshi has no hard cap, but liquidity drops off significantly past 3-4 legs. Fanatics Markets caps combos at 4 picks. As a practical matter, 2-3 legs is the sweet spot for getting competitive RFQ pricing. Beyond that, the market maker’s spread widens and can erase the structural advantage over a sportsbook parlay.

🛡️ Responsible trading

Combo trades are high-risk by design. Every leg must hit for the combo to pay out, which means the probability of winning drops with each leg you add. A 3-leg combo of 50/50 contracts has a 12.5% chance of paying out. A 4-leg combo: 6.25%. The potential return is attractive precisely because the probability of collecting it is low. Never trade combos with money you cannot afford to lose, and be especially cautious with low-probability, high-payout positions where the entertainment value may outweigh the expected mathematical return.

🛡️ Responsible Gambling Resources: If you or someone you know is struggling with gambling, help is available. Contact the National Council on Problem Gambling or call 1-800-GAMBLER. You can also text “GAMBLER” to 1-800-426-2537. Set deposit and loss limits before you start trading.