The U.S. runs the most sophisticated financial derivatives markets on the planet. Trillions in interest rate swaps and oil futures and currency options trade every day, much of it overseen by a federal agency most Americans couldn’t name if you spotted them the first two letters.

And yet for most of modern history, if you wanted to put $50 down on who will win the presidential election, you had to do it with a bookie, a buddy, or an offshore website based in Dublin.

That’s basically the tension that has defined prediction market regulation in this country. What is betting? What is investing? The gray area dominates the conversation today, as markets where you trade on the outcome of events (elections, Fed decisions, sports results, MrBeast videos, what the president will say, and virtually anything you can conceive) sit in a weird middle ground. Are they financial instruments? Or are they gambling? Depending on who you ask and what time of day it is, the answer changes.

Here’s how we got where we are. It’s a story of academic experiments, offshore cowboys, federal licenses, state-level pushback, and a handful of lawsuits that will shape the industry for years.

For the bulleted version, see our U.S. prediction markets: modern timeline. What follows is the narrative.

Sitting at the bar

Americans have been betting on elections for a long time. Wall Street-adjacent markets took real money on presidential races from the late 1800s into the 1940s. But the modern electronic version was born out of a 1988 conversation at a bar near the University of Iowa.

Three professors, Robert Forsythe, Forrest Nelson, and George Neumann, were kicking around the idea of using real-money markets to forecast elections. The polls had just blown the Michigan Democratic caucus, missing Jesse Jackson’s surprise win. The professors thought they could do better.

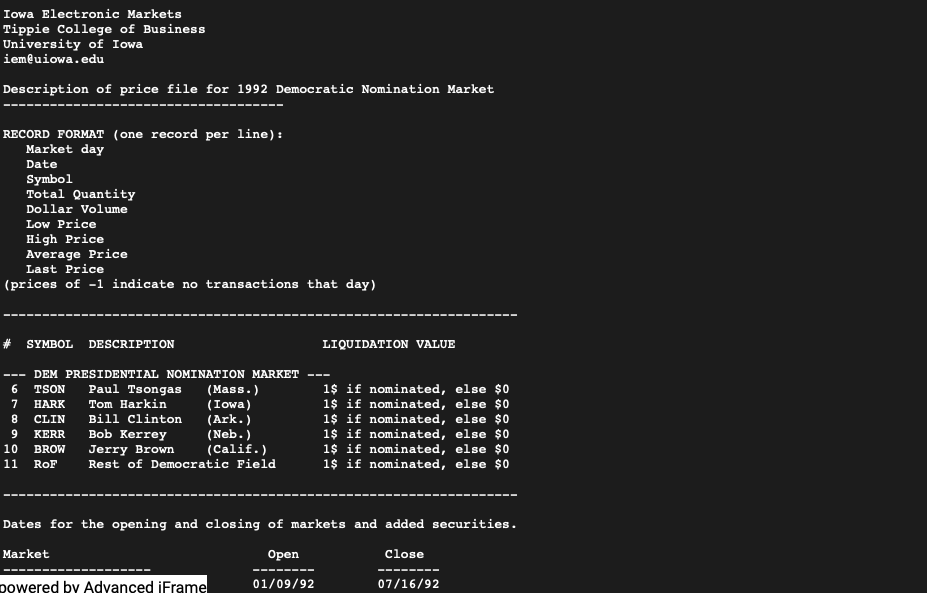

They launched the Iowa Electronic Markets later that year. The Commodity Futures Trading Commission (CFTC) staff granted no-action relief in the early 1990s, including a 1993 letter, letting the project continue under tight academic limits: a $500 participant cap plus limits on the number of traders in each submarket. The whole thing was explicitly academic, run by what’s now the University of Iowa’s Tippie College of Business.

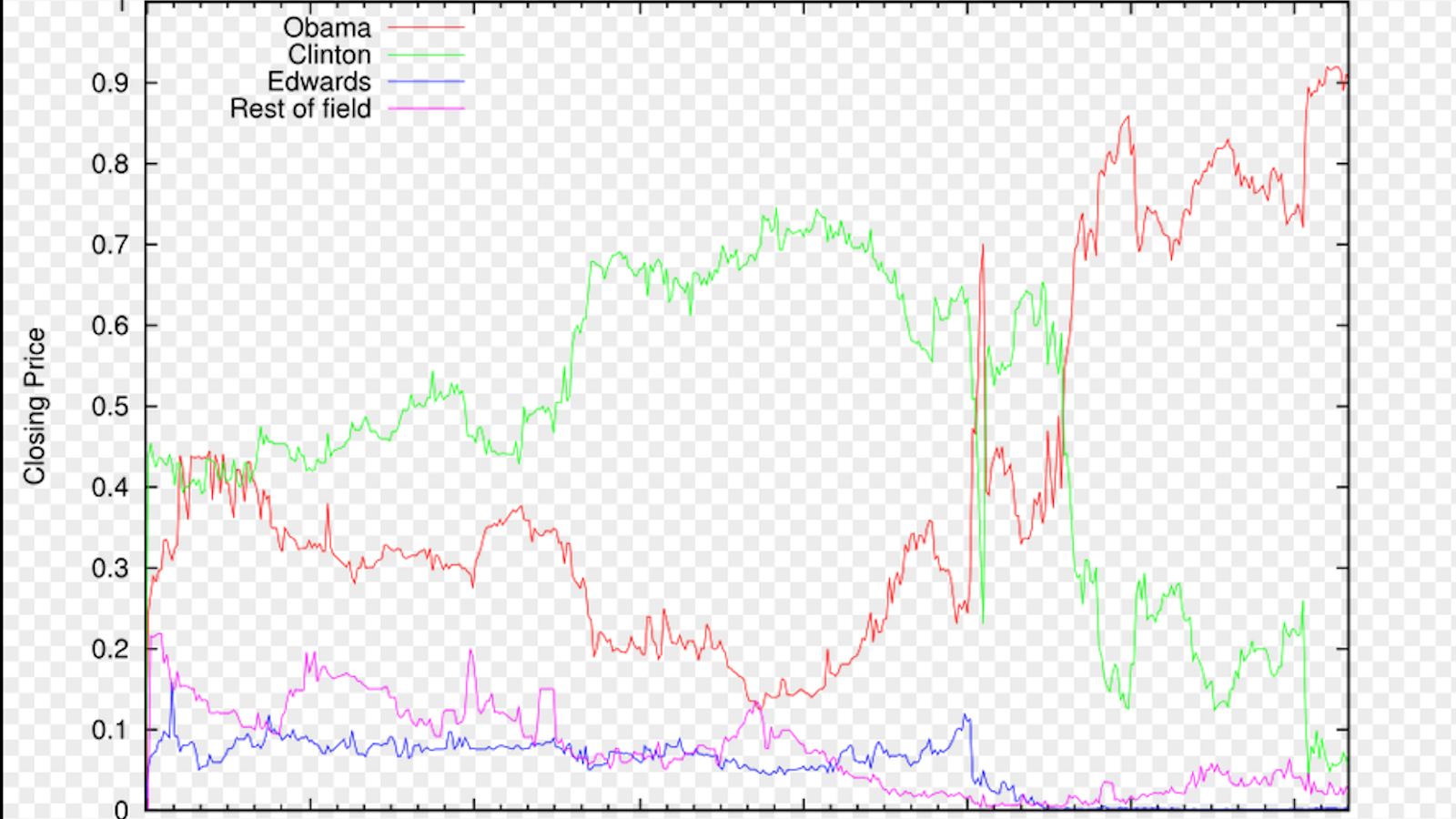

What happened next surprised a lot of people, including economists. The IEM worked. Really well. A 2008 study looked at nearly 1,000 polls across five presidential elections between 1988 and 2004 and found the markets beat the polls about 74% of the time. Average prediction error on election eve was often around 1.3 percentage points.

🔑 Why this matters: By framing itself as research, running under CFTC no-action relief, and staying small, the IEM set the blueprint for a real-money prediction market in the U.S. Every platform that came later either followed it or tried to get around it.

The offshore era

By the early 2000s, the internet had made prediction markets scalable in a way academic experiments couldn’t match. Enter Intrade, an Irish company based in Dublin that happily took bets from American users on everything from presidential elections to Oscar winners to the price of gold.

Intrade wasn’t academic. At all. It was a commercial prediction market operating offshore and outside the reach of regulators, and for about a decade it was the place to go if you wanted to put real money down on U.S. events. During the 2004 and 2008 presidential cycles, its odds got cited everywhere. News networks started treating its numbers like polling data. It looked like Intrade had cracked the code.

It hadn’t.

In November 2012, the CFTC sued Intrade in federal court in Washington, D.C., for violating U.S. rules on off-exchange options trading. Intrade cut off American users within days. Four months later, in March 2013, it suspended all trading worldwide, citing “financial irregularities.” Intrade’s CEO, John Delaney, had died attempting to climb Mount Everest in 2011, and an investigation later turned up more than $2 million in insufficiently documented payments tied to accounts controlled by Delaney.

So the Intrade era ended with a regulatory shutdown followed by a financial scandal. Not the cleanest exit. The bigger lesson for the industry was this: the CFTC was willing and able to go after offshore platforms that served U.S. customers. Running the business from Dublin was not a long-term plan.

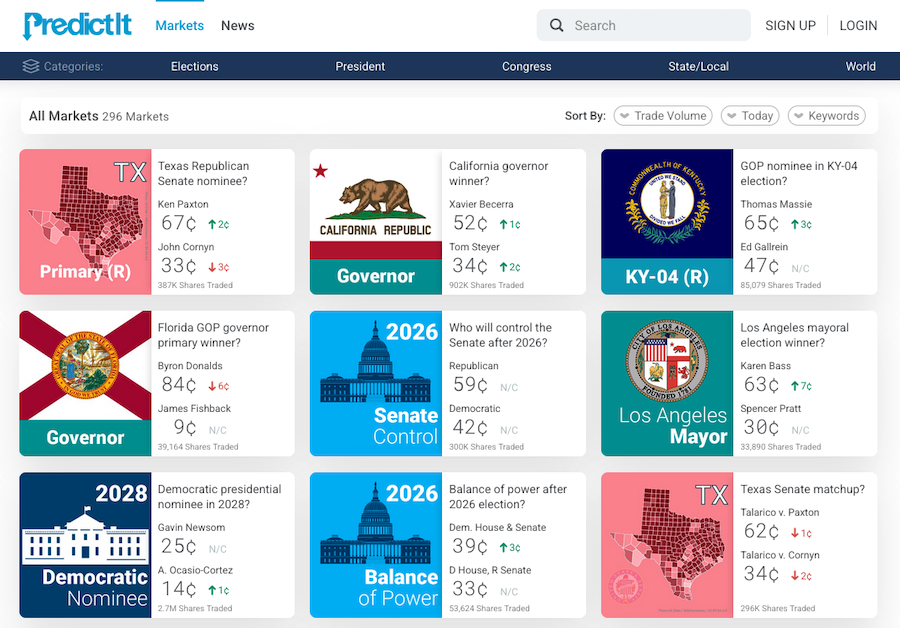

PredictIt

Into the vacuum stepped PredictIt, a political prediction market run by Victoria University of Wellington in New Zealand. PredictIt got a CFTC no-action letter in 2014 for a small-scale, not-for-profit academic market. The limits: $850 max per participant in any given contract, 5,000 traders max per contract, and contracts limited to political events or economic indicators.

Those limits mattered. An $850 cap kept out institutional money and serious speculators, but it was big enough that regular people could participate. For roughly eight years, PredictIt was the de facto U.S. political prediction market. If you saw odds on the 2016 or 2020 races quoted in a news story, there was a decent chance they came from PredictIt.

The structure had a downside. Critics argued the tight limits could distort prices, especially once popular contracts hit the trader cap and new participants couldn’t get in. And the academic-framing-as-legal-cover model turned out to be fragile.

In August 2022, the CFTC revoked PredictIt’s no-action letter, claiming the platform had failed to comply with its terms. The move was sudden, the reasoning was thin, and it prompted a lawsuit. A federal court issued an injunction letting the platform keep operating while the case proceeded. Members of both parties pushed back publicly. The CFTC’s case, it turned out, wasn’t great.

The fight dragged on for three years. In July 2025, a federal judge ruled in PredictIt’s favor, and shortly after, the CFTC and PredictIt settled. Position limits went from $850 to $3,500. The 5,000-trader cap was eliminated. Two months later, the CFTC designated Aristotle Exchange DCM, Inc. as a regulated exchange and approved related Aristotle clearing operations.

Kalshi time

The big shift came in November 2020, when the CFTC granted a Designated Contract Market license to Kalshi, a prediction market startup founded by two MIT alumni, Tarek Mansour and Luana Lopes Lara. Mansour had done stints at Goldman Sachs and Citadel. Lopes Lara had worked at Bridgewater, Citadel, and Five Rings.

Kalshi was the first modern prediction-market startup built around event outcomes to get a DCM license. HedgeStreet (later Nadex) had been a DCM listing event contracts since 2004. But Kalshi was the first of the current generation to clear the full designation process.

A DCM license is a different animal than a no-action letter. A no-action letter is the CFTC staff saying it won’t enforce as long as you stay within certain lines. A DCM license is the real thing. The CFTC has reviewed your structure, rules, and compliance systems, and signed off. Individual contracts you list still have to pass muster, either through CFTC review or through self-certification the agency can later challenge. But you’re a regulated exchange, operating under the Commodity Exchange Act.

📌 Key distinction: DCM status also gave Kalshi something else: a foundation to argue that federal law preempts state gambling law. Kalshi and the operators that followed would lean hard on that argument a few years later. For more on how Kalshi works in practice, see our full Kalshi review or our Kalshi bonus page to get started with a $10 trading credit.

The first real test came over political contracts. Kalshi wanted to list markets on which party would control Congress. In September 2023, the CFTC blocked the contracts, saying they involved gaming, activity unlawful under state law, and were contrary to the public interest under Section 5c(c)(5)(C) of the Commodity Exchange Act. That provision, added by the Dodd-Frank Act in 2010, gives the CFTC discretion to prohibit event contracts involving gaming, terrorism, assassination, war, or activity that’s illegal under state or federal law.

Kalshi sued. In September 2024, a federal district court ruled in Kalshi’s favor, holding that the congressional-control contracts didn’t “involve” gaming or unlawful activity the way the CFTC had interpreted the statute. The D.C. Circuit denied the CFTC’s emergency stay in October 2024, and political markets went live before the presidential election. The CFTC later moved to drop its appeal in May 2025.

Sports and states

This is the part where things got interesting. And by interesting, we mean chaotic.

In December 2024, Crypto.com started offering sports event contracts. Kalshi followed in January 2025. The pitch was the same as with politics: these are federally regulated derivatives, not gambling, and the CFTC’s jurisdiction preempts state gambling law. If that distinction feels blurry to you, you’re in good company. We break it down in our prediction market vs. sportsbook comparison.

State gaming regulators did not agree.

The response was fast. New Jersey, Nevada, Maryland, Massachusetts, Ohio, Arizona, and a growing list of other states sent cease-and-desist letters, opened enforcement actions, and filed lawsuits. The state argument: sports event contracts are functionally the same as sports betting, and CFTC-regulated exchanges can’t opt out of state law by calling it something else.

Kalshi’s legal play has generally been to challenge state actions on preemption grounds, mostly in federal court. The results have been a mixed bag, and the map has shifted fast. For the latest on every active case, see our Kalshi litigation coverage.

Early on, Kalshi looked like it was winning. In April 2025, federal district courts in Nevada and New Jersey granted preliminary injunctions, finding Kalshi was likely to succeed on its argument that sports event contracts are swaps under the CEA and that state enforcement is preempted.

Then the map got messier. In August 2025, a Maryland federal court denied Kalshi’s bid for a preliminary injunction. Nevada flipped hard in November 2025, when a federal judge lifted the earlier injunction, and a Nevada state judge later blocked Kalshi’s sports activity in March and April 2026. Massachusetts won an injunction against Kalshi. Arizona brought criminal charges, though a federal judge later paused the prosecution. In March 2026, an Ohio federal judge denied Kalshi’s preliminary-injunction request, rejecting the swap argument and letting Ohio enforcement move forward.

Kalshi got wins in the same stretch. A federal judge in Tennessee granted Kalshi preliminary relief in February 2026. And in April 2026, the Third Circuit affirmed the New Jersey preliminary injunction, giving the industry its first federal appellate-level win, though still not a final nationwide ruling.

⚠️ Head’s Up: The state-by-state picture is genuinely complicated and changes frequently. For the current status in your state, check our Kalshi state-by-state legality guide. For the broader federal-vs-state conflict, see our analysis of the states rights vs. federalism battle.

Then the federal government jumped in. On April 2, 2026, the CFTC and Justice Department sued Arizona, Connecticut, and Illinois, seeking to block state enforcement against CFTC-registered operators and establish federal preemption. A federal court in Arizona issued a temporary restraining order a week later, pausing the state’s criminal case against Kalshi.

Meanwhile, the market kept growing. In August 2025, CME Group announced a FanDuel partnership to develop a standalone prediction market app. DraftKings announced its own plans later that year after acquiring Railbird. Both apps launched in December 2025: DraftKings Predictions on December 19 and FanDuel Predicts on December 22, both running on CME Group contracts. Sports-event contracts were limited to states without legal online sports betting, though DraftKings’ broader app offered non-sports contracts in additional states. The sportsbook operators’ thinking was straightforward. If prediction markets were going to eat their lunch in non-legal states, they might as well be the ones serving it. For a side-by-side look at how all these platforms stack up, see our best prediction market sites rundown.

Nevada didn’t appreciate the two biggest U.S. sportsbooks offering what it considered unlicensed sports betting. In November 2025, the Nevada Gaming Control Board accepted Flutter’s surrender of its registration and related FanDuel licenses, and granted DraftKings’ request to withdraw its pending Nevada sports-wagering applications, citing the operators’ prediction market plans. Both companies then relinquished their American Gaming Association memberships over the split.

More on the state fights: Kalshi’s state-court lawsuits and the states-vs-CFTC battle.

Congress gets involved, sort of

Congress has been a special guest star in all this, and certainly not a full-time cast member.

The 2010 Dodd-Frank Act is where the current statutory mess starts. Section 5c(c)(5)(C) gives the CFTC discretion to prohibit event contracts involving gaming and a handful of other activities if the agency decides they’re contrary to the public interest. When the law was written in 2010, PASPA still blocked most state-authorized sports betting. Nevada ran full sportsbooks. A few other states had limited grandfathered sports wagering. Almost everywhere else, it was flat-out illegal. Against that backdrop, sports-event contracts in 2010 looked a lot more like gambling than finance. A lot has changed since then, but the statutory text has not.

There have been various legislative proposals to clarify the status of event contracts since, some pro-platform, some very much not.

The executive branch has mattered too. The CFTC’s stance has swung sharply between administrations. The Biden-era CFTC was aggressive against prediction markets. The Trump-era CFTC, first under Acting Chair Caroline Pham starting in January 2025, and then Chairman Michael Selig after his December 2025 swearing-in, took a friendlier approach. It dropped the Kalshi election-contract appeal, didn’t move to halt self-certified sports contracts across the board, and signaled that the gaming and preemption questions were going to get sorted out in court, not at the agency.

Where the industry lands depends less on CFTC rulemaking than on how federal courts resolve preemption. That’s slower, and it’s nowhere near done.

Where we are, and what’s next

The current moment is probably the most consequential in the industry’s history. Prediction markets are mainstream in a way they’ve never been. CME and the two biggest U.S. sportsbooks are in the business. Kalshi has been valued at roughly $22 billion. PredictIt is back. Polymarket is returning through its regulated Polymarket US/QCX pathway. Robinhood has integrated event contracts into its app. Crypto platforms and sportsbooks have piled in.

At the same time, the legal foundation underneath all of it is still being poured. The preemption question is unresolved across the country. Kalshi holds a major Third Circuit win in New Jersey but faces adverse rulings elsewhere. States certainly aren’t giving up. In April 2026, New York Attorney General Letitia James sued Coinbase and Gemini over their prediction-market offerings, calling them illegal gambling under state law. Congress could step in. Courts could split further. The commercial expansion is running ahead of the legal clarity, which is how these things usually go. Move fast, break things.

A few questions will shape what comes next. Does CEA preemption of state gambling law hold up if the Supreme Court takes a case? Does Congress clarify, or restrict, the CFTC’s jurisdiction? Does industry success build enough political muscle to lock in the current framework before the next administration can unwind it?

The answers will decide whether the next decade of U.S. prediction markets looks more like regulated finance or state-by-state gambling. Both outcomes are on the table.

The first few decades of American prediction market history were written by three professors at a bar, an Irish exchange that imploded, and a New Zealand university trying to run a political experiment. The next chapter is being written by federal courts and lawyers in expensive suits. Either way, it’s a wilder story than most people realize.

Related InGame coverage

- U.S. prediction markets: a modern timeline

- States rights vs. federalism: can prediction markets be kept at bay?

- Kalshi litigation coverage

- Kalshi review

- Polymarket review

- Kalshi vs. Polymarket: which prediction market is better?

- Best prediction market sites for sports betting in 2026

- Prediction market vs. sportsbook: what’s the difference?

- Peer-to-peer sports betting: how does it work?

- Prediction market fees, explained

- Investment, new players pour into prediction markets